Skip to main content

Skip to main content

Key takeaways:

- Digital wallets are becoming the main way users with smartphones purchase goods, pay for services, and store documents.

- The digital wallet market is full of competitive general-purpose solutions, but many businesses still build custom apps.

- A custom digital wallet helps businesses better target customers, secure sensitive financial data, and comply with strict regulations.

- Building a custom wallet requires deep market research and business analysis, as well as development, QA, and cybersecurity expertise.

Many people already use digital wallets as their primary way of managing their finances. Developing digital wallets allows businesses to be closer to their clients, simplify access to their services, and reach new markets. However, strong competition and strict security requirements make wallet development challenging.

In this article, we take a look at reasons for investing in custom digital wallet development and discuss how to create a digital wallet. This article will be useful for technical leaders of banks, FinTech companies, and businesses that want to provide customers with quicker access to their services.

Contents:

Why FinTech businesses need custom digital wallets

A digital wallet is a mobile, web, or cross-platform application that contains sensitive information needed to authenticate a user in payment services and facilitate purchases. Gartner predicts that by 2026, at least 500 million smartphone owners will regularly use digital wallets.

Goals and features of digital wallets differ depending on the provider. Apps like Walmart Pay and Amazon Pay simplify access to specific services, making it easier for customers to manage purchases, subscriptions, and payment preferences. Wallets like Venmo and Cash App enable peer-to-peer payments and personal finance management without focusing on a specific service. Some apps like Google Wallet allow users to manage documents like IDs, concert tickets, and boarding passes as well as payment cards.

Despite such a variety of available solutions, many businesses choose to invest in custom FinTech app development. Here’s what they gain from creating a custom wallet:

- Improve the user experience (UX). A custom app can deliver features specific to different groups of users or operational needs. For example, your digital wallet may store specific types of documents or simplify peer-to-peer transactions.

- Provide more engaging services. A digital wallet provided by a business usually helps users interact with the business’s services in a couple of clicks. Also, digital wallet apps make it easier for businesses to implement and track bonus programs.

- Enhance the security of private data. Wallets constantly process users’ sensitive personal and financial information, but not all apps on the market can ensure reliable data protection. Delivering a custom wallet allows your business to ensure the security of your customers’ data and compliance with cybersecurity requirements.

- Reach new clients and markets. Providing a digital wallet is a convenient alternative to producing and shipping physical cards. This type of app can help you reach new markets where you aren’t represented physically.

To maximize these benefits, make sure that your custom digital wallet has all the features required by your business and clients. You can start by selecting the type of wallet to develop. We’ll overview the key types in the next section.

Partner with an experienced FinTech development company!

With expertise in data management, cybersecurity, and cross-platform development, Apriorit teams are perfectly suited to build the exact app you envision.

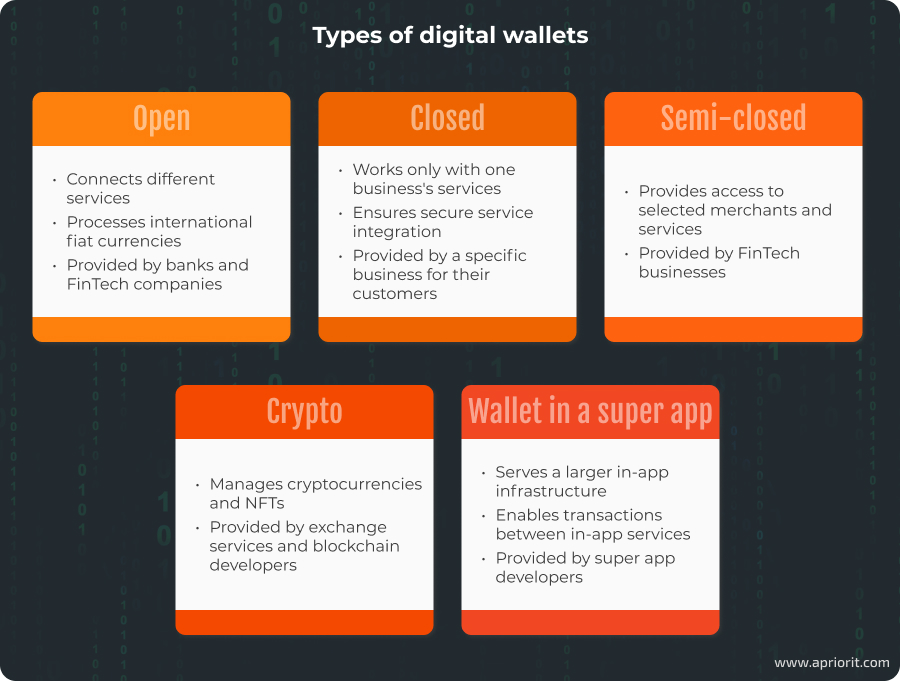

5 types of digital wallets

The type of digital wallet you should build depends on the type of funds you want it to manage (fiat currencies or crypto), the target feature set, legal and regulatory requirements, and the wallet’s place in your infrastructure. Usually, companies choose one of these types of digital wallets:

Open wallets. The most flexible type of wallet app, an open wallet allows users to store funds, make payments, withdraw money, and make transactions between different banks and services. Open wallets don’t limit a user to one banking provider. Many also support international transactions, making them a preferred choice for users who travel. Such apps are often developed by banks themselves or by FinTech companies in partnership with banks. PayPal, Apple Pay (in some regions), and Google Pay are well-known examples of open wallets.

Closed wallets. A closed wallet is designed for transactions within a single company’s ecosystem. Using a closed wallet, users can add funds to their accounts, receive store credits or refunds, participate in bonus programs, and pay for goods and services of the wallet-issuing company. A closed wallet makes it easy for customers to interact with a business. It also allows the business to retain customer spending within their ecosystem and ensure secure integration between elements of that ecosystem. Examples of closed wallets are Starbucks Wallet and Walmart Pay.

Semi-closed wallets. This type of wallet offers more flexibility than a closed wallet, while having some restrictions on access to services and processes. Users can load money into a closed wallet account and make purchases at selected merchants that have agreements with the wallet provider. Unlike open wallets, semi-closed wallets typically don’t allow withdrawals as cash or transfers to a bank account. This model is commonly used in mobile payment ecosystems where businesses want to encourage in-app transactions while still allowing spending across multiple brands. Services like Paytm Wallet and M-Pesa operate in this space.

Crypto wallets. Unlike traditional digital wallets that store fiat currency, a crypto wallet is designed to hold digital currencies or NFTs. These wallets operate on a blockchain rather than through banks or financial institutions. Some crypto wallets are custodial, managed by third-party providers like exchanges, while others are non-custodial, giving users full control over their private keys and funds. Popular crypto wallets such as MetaMask and Trust Wallet, and hardware wallets like Ledger offer varying levels of security and accessibility for cryptocurrency users.

Wallets in super apps. Some digital wallets operate as part of super apps — platforms that combine multiple services like payments, ride-hailing, food delivery, and shopping. Integrating a wallet into such an app allows users to make financial transactions without ever leaving the app. Unlike standalone digital wallets, which focus purely on payments, super app wallets provide a more engaging user experience, increasing customer retention. WeChat Pay, GrabPay, and Gojek Wallet are the most well-known examples.

Each type of digital wallet plays a distinct role in the financial ecosystem, offering different levels of access, security, and integration. While having different use cases, however, they share some core properties. Let’s take a look at features any custom digital wallet should have.

Read also

Mobile Banking App Development: Benefits, Features, and Challenges

Learn how a banking app is different from a wallet, the benefits of developing one, and how you can get started.

Must-have features for a digital wallet

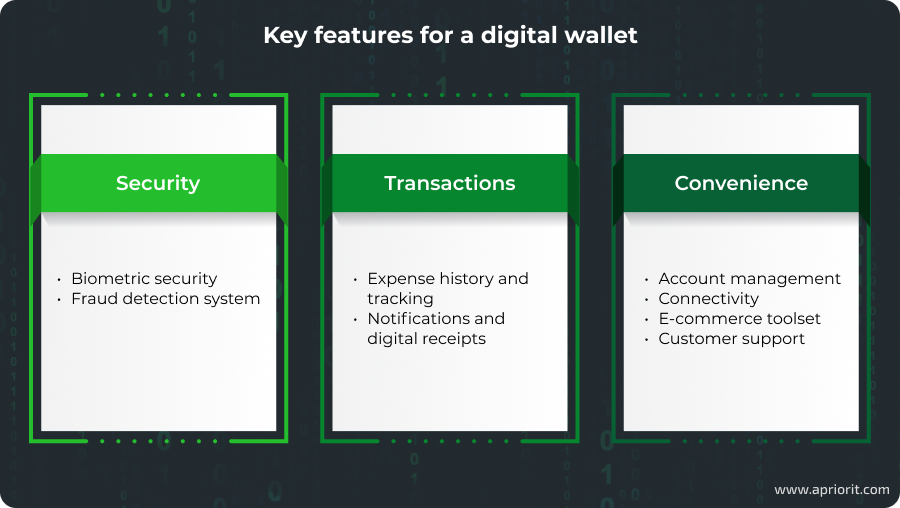

Before building a digital wallet, it’s best to research the features your app needs. This research should be based on market trends, user needs and preferences, and your business requirements. Below, we list usual features for digital wallets that you can start with.

Biometric security. Biometric authentication based on fingerprint scanning, facial recognition, and even voice authentication helps prevent unauthorized access while also reducing reliance on passwords and PIN codes. It greatly increases the protection of your wallet from identity, data, or device theft. Biometric authentication also improves the user experience, as users are not forced to remember a complex password.

Fraud detection system. Many wallets incorporate data analytics and AI-driven systems that analyze transaction patterns to identify suspicious activity, trigger alerts, and sometimes even block transactions until the user verifies their legitimacy. These systems help prevent unauthorized transactions and identity theft.

Expense history and tracking. Users expect their digital wallets to track and manage their spending. Built-in expense tracking allows users to view transaction histories, categorize spending, and set budgets. Some wallets integrate financial analytics and reporting features that provide insights into spending habits.

Notifications and digital receipts. Real-time notifications keep users informed about transactions, upcoming payments, and security alerts. Digital receipts provide a convenient way to store proof of purchase without the need for paper receipts, making them valuable for both tracking personal finances and managing business expenses.

Account management. A digital wallet should allow users to manage one or multiple accounts, letting them add payment methods, track spending, and configure alerts and security features for each account. This flexibility is particularly important for business users and frequent travelers who need to switch between accounts seamlessly.

Connectivity. A digital wallet’s ability to facilitate quick and secure transactions depends on its connectivity options. Most modern wallets support Near Field Communication (NFC) for contactless payments, QR code scanning for instant transfers, and Bluetooth-based payments for proximity transactions. These features ensure smooth integration with retail POS systems, online stores, and peer-to-peer transactions.

E-commerce toolset. E-commerce tools extend the functionality of wallets integrated with marketplaces or super apps beyond payments. Features such as automated commission handling, billing and invoicing, and integrated feedback help facilitate transactions between buyers and sellers.

Customer support. When something goes wrong with their finances, users need quick and professional help. Many digital wallets now feature in-app chat support and AI-powered virtual assistants. Whether resolving disputes, answering security concerns, or guiding users through complex transactions, customer support tools enhance users’ trust and engagement.

Note: These are only the basic features that users expect a digital wallet to have. You’ll want to add more features tailored to your business needs and based on user research.

To build a custom digital app, follow the process we discuss in the next section. We’ll take a look at development stages and challenges to pay attention to.

Related project

Building AWS-based Blockchain Infrastructure for International Banking

Explore the story of a US-based company who requested Apriorit’s engineering assistance and received a custom blockchain system for banking and governmental organizations.

How to develop a custom digital wallet app

Digital wallet app development generally follows a typical software development lifecycle. Below, we analyze how Apriorit approaches a project, discuss key activities for each stage, and offer advice to ensure project success.

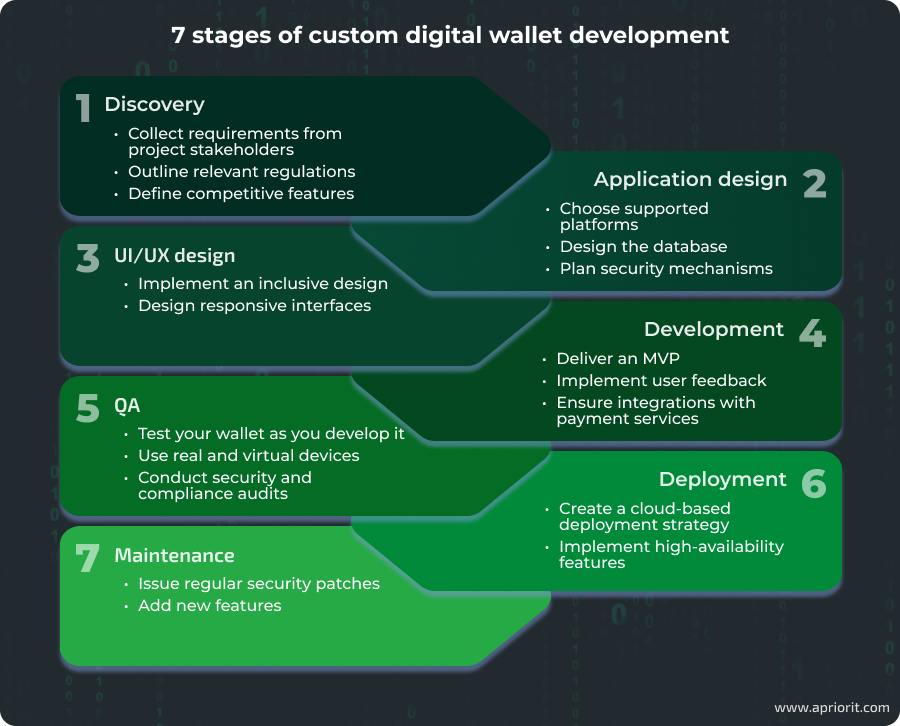

1. Discovery phase

The initial phase of development focuses on defining the wallet’s core functionality, understanding market demands, and outlining compliance requirements. Project managers and business analysts document this information to form a shared vision of the project among all team members. Later in the process, this documentation will help the team be on the same page and deliver the application end users expect.

Regulatory requirements for digital wallets vary depending on the target market and the type of wallet. In the EU, such apps usually must comply with PSD2 and the GDPR, while those operating in the United States must comply with PCI DSS and the CCPA. These requirements influence everything from data encryption standards to authentication mechanisms and cross-border payment processing.

Defining the wallet’s competitive features is another challenge during the discovery phase. With numerous digital wallets on the market, you should choose your functionality wisely to make sure your app has unique competitive features. Some wallets prioritize multi-currency support and integration with decentralized finance platforms, while others focus on AI-driven financial insights and business payment automation.

2. Application design

At this stage, the development team plans everything about the future application: supported platforms, centralized or distributed storage, money processing mechanisms, and security considerations. Essentially, they create a blueprint for further development. A well-planned application architecture allows your team to avoid costly rework, precisely estimate their work, and deliver a reliable and protected application.

When choosing supported platforms, analyze how your users prefer to interact with the app. While mobile applications dominate the digital payments market, web-based wallets and desktop versions are necessary for enterprise users. You can also look into cross-platform development with frameworks like Flutter or React Native.

The choice between a centralized or distributed architecture significantly impacts security, transaction speed, and data storage. A centralized approach simplifies transaction processing and compliance management but introduces a single point of failure, making robust cybersecurity measures essential. A distributed architecture, often used for crypto wallets, offers enhanced security through decentralized transaction verification but presents challenges in regulatory compliance and performance optimization due to blockchain network constraints.

Security considerations must come from applicable compliance requirements and best practices in your field. Digital wallets require advanced encryption methods such as AES-256 and TLS 1.3. Tokenization replaces sensitive card data with randomly generated tokens, reducing exposure to fraud. Multi-factor authentication and anomaly-based risk scoring help prevent unauthorized transactions.

3. UI/UX design

A digital wallet’s interface must provide a seamless experience. Designing a responsive user interface (UI) that adapts to different devices and screen sizes is one of the key challenges, especially for cross-platform wallets. The UI should accommodate different interaction patterns, from NFC-based contactless payments to QR code scanning and biometric authentication, without compromising speed or usability.

Inclusive design is another UI/UX practice to adopt. It ensures accessibility for users with special needs, requiring compatibility with screen readers, voice-based navigation, and customizable visual elements for individuals with color blindness or low vision.

Read also

Building a Cross-Platform Mobile Web Application with Ionic and Angular

Get an overview of Ionic and Angular from Apriorit experts. Explore how to combine these two frameworks to build a flexible and seamless cross-platform app.

4. Development

It’s a good practice to start the development stage with delivery of a minimum viable product (MVP) that includes core wallet functionality and security mechanisms. An MVP helps you validate technical choices, check alignment with user expectations, and confirm the competitiveness of your product before investing in it fully. With an MVP, you get a platform that you can augment with new features and capabilities in the future.

Once you have a successful MVP, there are several aspects to pay attention to during development:

- Security features like industry-standard authentication protocols, end-to-end encryption, and tokenization

- Know Your Customer (KYC) procedures powered by automated identity verification services, integrating document scanning and biometric checks

- Fraud detection systems powered by data analytics or AI that comply with relevant anti-money laundering regulations

- Integration of payment processing systems, gateways, and third-party and custom banking APIs for all services your users may require

- Smart contracts and decentralized infrastructure to process cryptocurrencies and NFTs

- Incorporating user feedback from the MVP

5. Quality assurance

Depending on the development framework you prefer, QA activities can happen alongside development or after it. At Apriorit, we prefer shift-left testing that allows for catching and fixing issues early.

When testing digital wallets, we pay attention to performance, usability, and security. For performance and usability testing, make sure to use both virtual devices and real devices. Mobile wallets must be tested under various network conditions, including in offline mode, to ensure uninterrupted functionality. Automated UI testing frameworks help detect inconsistencies in user interactions, while manual testing on real devices ensures flawless work of biometric authentication and NFC-based transactions.

Security and compliance audits must be conducted before deployment to identify vulnerabilities in authentication flows, data storage, and transaction handling, as well as the app’s adherence to regulatory requirements. You can include penetration testing in your audit process to simulate cyber attacks and uncover weaknesses in the system. Once your team fixes all the issues discovered by these audits, the app is ready to go live.

6. Deployment

Launching a digital wallet requires coordinating compliance approvals, infrastructure readiness, and distribution through app stores or enterprise deployment channels. Cloud-based deployment strategies often rely on containerized microservices using Kubernetes and Docker to ensure scalability and resilience.

High-availability architectures with automated failover mechanisms prevent downtime, while continuous monitoring systems detect and respond to performance or security incidents in real time. Issues inevitably arise during deployment, but with quality development and QA, you can limit them.

7. Maintenance and support

Post-deployment support is essential to maintaining a wallet’s competitiveness, security, and user satisfaction. Regular security updates help address emerging threats and vulnerabilities, and new features can be added to satisfy new compliance requirements.

Developing a digital wallet requires expertise across multiple domains, from security engineering to UX design and AI model implementation. Addressing challenges at each stage of development ensures a scalable, secure, and user-friendly payment solution that meets the demands of modern financial ecosystems.

Read also

How to Ensure Your Mobile Banking App’s Security: Tips and Best Practices

Mobile banking apps process a lot of sensitive data, making them prime targets for hacking attacks. Learn about the key threats to such apps and Apriorit’s take on securing mobile banking.

How Apriorit can help you develop a digital wallet

Leverage Apriorit’s experience in FinTech, mobile, and cloud development to build the product you envision without delays and without going over budget. We can augment your team with specialists you lack, or provide you with a full team of development and QA experts who will quickly adjust to your business processes.

Here’s why we’re a reliable partner for custom digital wallet development:

With our skilled business analysts, engineers, and QA specialists, you can deliver a competitive and secure digital wallet that your users will enjoy.

Conclusion

Creating a digital wallet is a complex process that requires deep expertise in security, compliance, and FinTech development. From implementing secure transactions to ensuring a seamless user experience, each stage presents unique challenges that demand careful planning and technical precision.

Apriorit development teams, skilled in mobile and web development, API integrations, and data management, can help you with any challenge your project presents. We’ll be glad to develop a digital wallet from scratch using your requirements. Leverage our years of FinTech experience to build the app you need.

Challenge us with your development project!

Apriorit teams are ready to help you with every step of your digital wallet development, delivering a competitive and reliable product.

Have a question?

Ask our expert!

Director of Global Markets Development